One of the reasons real estate is an appealing option for many investors is the tax advantage it can offer over other investment forms. One method of capitalizing on the tax benefits is purchasing properties in Opportunity Zones. This is a newer investment form, having been created in the recent Tax Cuts and Jobs Act of December 2017, which means that many investors still have a lot of questions about how exactly Opportunity Zones work.

I wrote a blog post back in October discussing some of the big picture components of Opportunity Zones including what the difference is between Opportunity Zones and Opportunity Funds and what the timeline is for capitalizing on these investments. In today’s post, however, I want to help clarify the actual steps you need to take in order to take advantage of this investment vehicle.

Benefits of Opportunity Fund Investment:

- Gains can be deferred until the sale of the investment or until December 31, 2026, whichever comes first.

- Ten percent of the capital gain can be excluded permanently if the OZ investment is held for five years. An additional five percent, for a total of 15%, can be excluded if the OZ investment is held for 7 years, or until December 31, 2026.

- The entire gain from the sale of the OZ investment can be permanently excluded if the investment is held for 10 years.

- Combination of incentives from State and local project incentives to offset project costs.

How to Qualify an Opportunity Zone Investment:

The investment must be made into a Qualified Opportunity Fund (QOF). The process to become a QOF is a self-certification process which requires completing an IRS form. No IRS approval is required.

The QOF may be organized as a corporation or a partnership and must hold at least 90% of its assets in OZ property. Investment into a QOF must be made within 180 days of recognizing a capital gain, which is similar to the 1031 exchange reinvestment window.

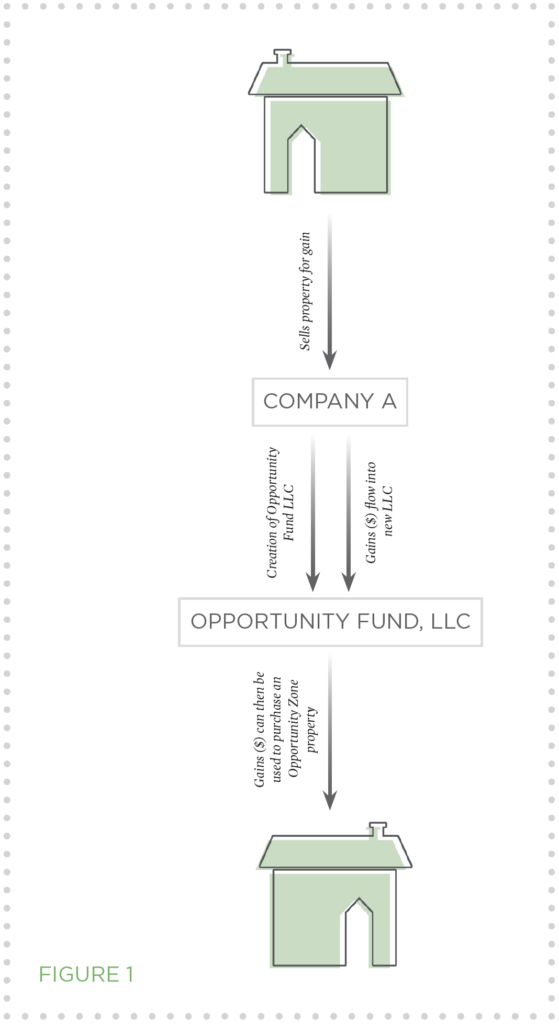

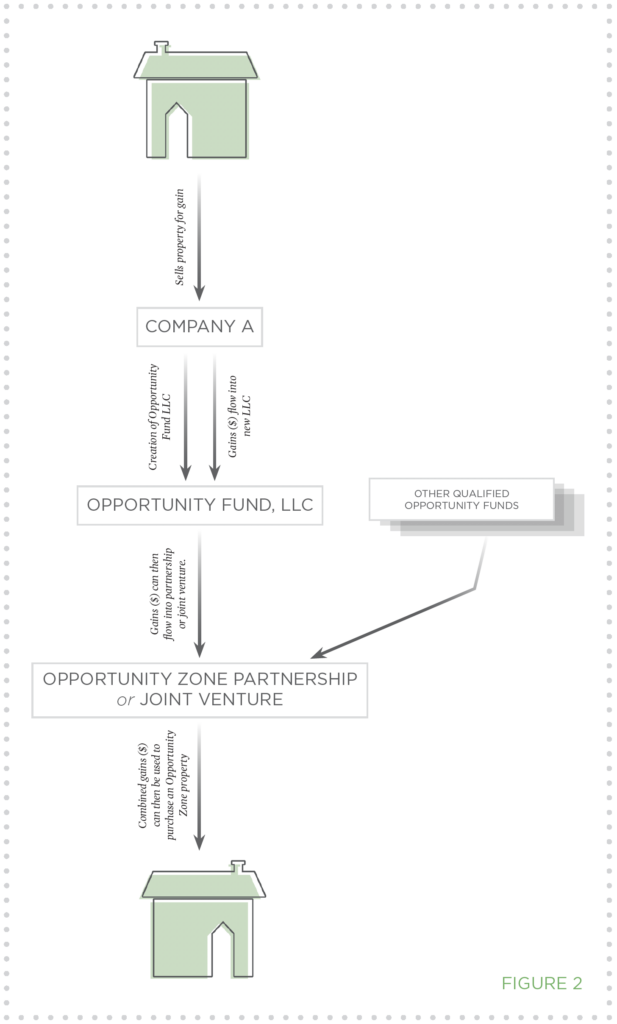

Opportunity Zone Process:

- Single Tier Purchase:

- Investor sells property for gain

- The gain flows into the investor’s original company

- Investor creates a QAF and the gain from the sale flows into this new LLC

- The QAF can then use the gains to purchase an Opportunity Zone property

- See Figure 1

- Double Tier Purchase:

- Alternatively, a QAF can partner with other investors in an Opportunity Zone Partnership or Joint Venture

- After the gains flow into the newly created QAF, an Opportunity Zone Partnership can be created

- The gains in the QAF can be combined with those of other QAFs

- The combined gains can then be used to purchase a property within an Opportunity Zone

- See Figure 2

Unsure whether investing in an Opportunity Fund makes sense for you? We recommend teaming up with a tax professional as well as a broker to make sure you are navigating this new investment vehicle correctly and capitalizing on all the potential tax benefits available to you!